The Asian Development Bank (ADB) on Thursday highlighted the raised India’s GDP growth forecast for the current fiscal year from 6.7 percent to 7 percent. It also stated the robust growth will be driven by robust public and private sector investment demand and improvement in consumer demand.

In the Asian Development Outlook, it mentioned that “The economy grew robustly in fiscal 2023 with strong momentum in manufacturing and services. It will continue to grow rapidly over the forecast horizon. Growth will be driven primarily by robust investment demand and improving consumption demand. Inflation will continue its downward trend in tandem with global trends, to boost exports in the medium term, India needs greater integration into global value chains.”

Mio Oka- ADB Country Director for India commented that “Notwithstanding global headwinds, India remains the fastest growing major economy on the strength of its strong domestic demand and supportive policies”.

Key points highlighted by ADB in the data analysis of the Indian Economy

-

Economic Performance

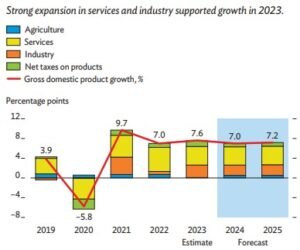

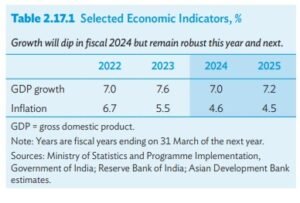

ADB has stated that Growth in India has increased to 7.6% in fiscal year 2023 which was driven by manufacturing, construction, and services. Agriculture growth dropped sharply due to the impact of erratic rainfall. This was compensated by an increase in manufacturing growth to 8.5%. Construction also grew rapidly by 10.7% due to strong housing demand. Services, which account for50% of GDP, grew by 7.5%, led by financial, real estate, and professional services.

Gross capital formation has also increased by 10.2% in FY2023 to contribute 3.4 percentage points to GDP growth as public and private sector capital expenditure grew strongly.

Exports also grew modestly at 1.5% in real terms, while imports grew by 10.9%, driven by greater domestic demand for inputs and capital goods. As a result, net exports declined, deducting 2.3 percentage points from growth.

Net indirect taxes also got a boost in FY2023 due to declining central government subsidy expenditure following high fertilizer subsidies in FY2022.

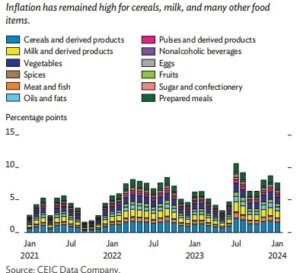

Food inflation has remained elevated, mainly from higher prices for pulses, vegetables, sugar, and cereals. Consumer inflation moderated in FY2023 despite higher food inflation.

Bank credit growth remained robust in FY2023, driven by demand for services and personal loans. The Indian rupee depreciated against the dollar by 1.1% in the first 11 months of FY2023. Government capital expenditure rose by 28.0% while current expenditure grew by only 2.5%. As a result, overall expenditure shrank as a share of GDP, even as receipts grew.

-

Economic Prospects

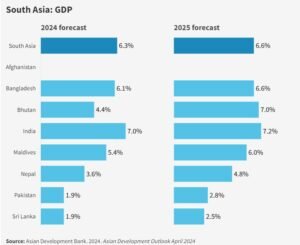

On balance, growth is forecast to slow to 7.0% in FY2024 but improve to 7.2% in FY2025.

Capital expenditure by state governments will also remain strong, helped by central government transfers to state governments for infrastructure investment.

On the private sector side, investment in housing will remain strong, driven by stable interest rates and higher income growth for high-income households.

The urban worker population ratio rose from 44.7% in the third quarter of FY2022 to 46.6% a year later, and the urban unemployment rate fell from 7.2% to 6.5%. Rural consumption was muted in FY2023 as rural incomes suffered from erratic rainfall affecting agriculture, as indicated by greater demand for work under the MGNREGA. Assuming normal monsoon rainfall, rural consumption will improve in FY2024.

India continues to benefit from improved competitiveness in digital services featuring higher value added, including through Indian global capability centers set up by multinational corporations. Imports will outgrow exports in FY2024,

driven by strong domestic demand especially for capital goods and intermediate goods.

The FY2024 central government budget set an aggressive deficit target of 5.1% of GDP and reiterated the fiscal

deficit target of 4.5% for FY2025. The government’s focus on fiscal consolidation will continue, creating space for private borrowing.

Less restrictive monetary policy and continued fiscal consolidation will pave the way for the rapid rate of increase in bank credit seen last year to continue in FY2024 andFY2025, notwithstanding regulatory tightening on unsecured personal loans.

The current account deficit will widen to 1.7% of GDP in FY2024 and FY2025 on rising imports to meet domestic demand. However, portfolio capital inflow will remain strong, attracted by the performance of India’s equity and debt markets.

Policy Challenge

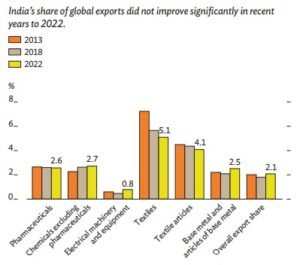

India’s growth strategy is predicated on substantial export growth. ADB has suggested that it can be achieved through integration into global value chains.

India participation in GVCs has been limited but on the other hand, India has been a global leader

in service trade. Its share of global service exports increased from 3.5% in FY2017 to 4.6% in FY2022. Further policy action is needed to improve India’s trade competitiveness and integration into GVCs. A simplified tariff policy is needed along with continued efforts to improve trade and logistics infrastructure has been exhorted by ADB.

Data on neighboring countries

As per the report, South Asia remains the fastest growing subregion as domestic demand improves on moderating inflation in most economies. It has recommended that Pakistan and Sri Lanka should recover from last year’s growth contractions.

- In Pakistan, growth is forecast rising at 1.9% in FY2024 (ending on 30 June 2024) and 2.8% in FY2025, up from the 0.2% contraction last fiscal year.

- In Sri Lanka, growth will rebound to 1.9% in 2024 and 2.5% in 2025 from the 2.3% contraction in 2023.

- In Bangladesh, garment exports will plunge growth up to 6.1% in FY2024 (ending on 30 June 2024) and 6.6% in FY2025.

- Hydropower investment and the commissioning of a major hydropower plant will drive growth in Bhutan.

- In Maldives, tourism and construction will boost growth in 2024 and 2025.

- Growth in Nepal will begin faster in FY2024 (ending in mid-July 2024) and FY2025 on rising domestic demand and hydroelectric output, and a continued recovery in tourism.

{kind=link}